Trump 2.0 and Solar’s Middle Market

Leading up to the 2024 presidential election, a GOP sweep of the presidency, house, and senate seemed like a worst case scenario for the US solar industry. Control of the legislative and executive branches would give Republicans an opportunity to use legislative measures as well as executive actions to roll back progress on renewables, including Biden's signature Inflation Reduction Act. And, with Trump in the White House again, who knows what chaos might ensue?

Now that this scenario has come to pass, it’s worth taking stock of how the election results are likely to affect solar’s middle market. We’ve previously covered the impacts of the IRA, the non-linear benefits of ITC percentages on project values, and the impacts of ITC transferability on the market. This legislation has supercharged solar’s middle market over the last two years and is the first focus of our attention here.

Reasons to be Optimistic

The key to keeping the Inflation Reduction Act intact, or at least the core provisions accelerating solar’s middle market, is the House of Representatives. House Speaker Mike Johnson has said that it would be impossible to repeal the full IRA, and the only way to change it is with “a scalpel and not a sledgehammer”. 18 of his House GOP colleagues have urged for this publicly, and many others have in private as well. SEIA and industry leaders have indicated that there is no political appetite for a full repeal.

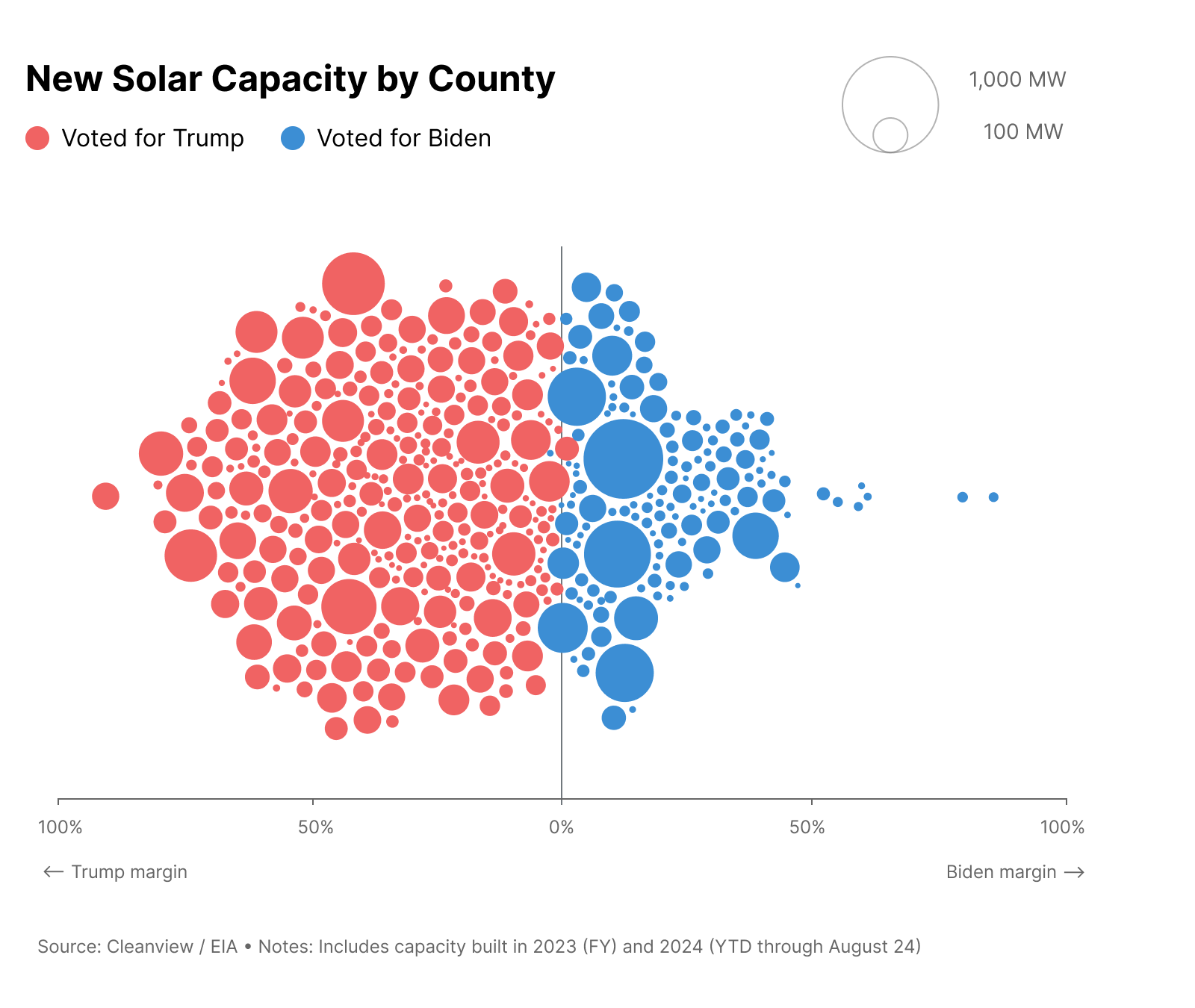

A big reason for bipartisan support for the IRA comes from its broad distribution of benefits across the country. The following chart illustrates how more solar capacity has been added in counties that voted for Trump than in counties that voted for Biden.

Historically, once a government program benefits certain constituencies it becomes very hard for Congress to take it away - especially when the constituency is broad and bipartisan. So there is good reason to be optimistic about the general stability of the Investment Tax Credit for solar projects.

Areas of Concern for the ITC

This all of course begs the question of what a “scalpel” would cut, and which parts of the IRA are most likely on the chopping block. Some of the top candidates for cuts do not affect solar’s middle market. These include EV tax credits and off-shore wind. Others would only impact specific types of projects in the middle market. These include the ITC adders for Low-to-Moderate Income communities and the direct pay or elective pay option for non-profit organizations.

The concept of Domestic Content aligns with GOP goals for US manufacturing, but it may become a requirement for the base 30% ITC on all projects instead of a bonus 10% adder to the tax credit. That would add costs for all projects while removing additional benefits for domestic components. We have not yet seen the Energy Communities adder considered as a priority for modification.

A greater long term risk to the middle market is the potential for an earlier phase-down of the tax credits, even as soon as 2027 or 2028. There are active discussions about this kind of timeline among the incoming administration. But it’s worth noting that such drastic changes have not passed congress, and seem rather heavy handed for a “scalpel” approach. If they are included, changes to the phase-down timeline may have the greatest impact on solar’s middle market in the long term.

The good news is that we may know how the IRA will change under Trump as soon as Q2 of 2025. Because of the way that the IRA was created, it can be modified through a budget reconciliation process. And this is likely to happen as part of a Republican effort to help pay for the extension of tax breaks from Trump’s first term, which are set to expire in 2025. Such a tax bill is part of a still broader Republican legislative agenda which faces considerable obstacles with a very slim house majority.

Other Areas of Concern

There will be tariffs on imports. And these do not require legislative changes and the approval of congressional representatives from the districts in the chart above. Despite a growing domestic manufacturing base, the US solar industry still imports most of its solar panels and inverters and will almost certainly be heavily hit by Trump’s tariffs, again.

The good news for the middle market is that distributed energy generation is much less impacted by tariffs than utility scale developments where the equipment makes up a larger share of project budgets. Tariffs will squeeze project economics across the board, but they are much more likely to make Gigawatt scale projects uneconomical than C&I, community solar, and small utility projects.

Grant programs are also candidates for the chopping block. And Trump will have broad authority to change political appointments at DOE and FERC. So forward-looking programs that support innovation and efforts at interconnection reform will likely be impacted, and may be stalled or derailed.

The Big Unknown

The biggest impact of a second Trump administration may come in the form of general uncertainty. This is terrible for business, especially in an industry built on long-term contracts. Despite the challenging changes ahead, we’ve heard a strong desire to get through them quickly so that we can once again know what we’re working with. Uncertainty can stall decision making, create delays, and sap momentum.

In his time away from the White House, Trump seems only to have enhanced his reputation as an agent for chaos. And he’s promising to deliver it in full force. So the biggest impact of Trump 2.0 may be what Donald Rumsfeld famously termed "unknown unknowns”.

How the Market is Reacting

So far, we’ve seen full steam ahead on deals in progress and strong interest in new deals on the horizon. The consensus is that good projects are likely to move forward, perhaps with some repricing and adjustments to accommodate legislative changes. This reflects industry optimism about the strength of the ITC and its broad support in the House of Representatives.

Reactions We’re Anticipating

In past rides on the solar coaster, we’ve seen accelerated market activity just prior to adverse policy or incentive changes followed by a slower period. Examples include previous ITC phase outs and the end of NEM 2.0 in California. We’re anticipating a similar pattern in the next few years, with its severity and timing determined largely by the extent of Republican trimming on the IRA. We could face a slower pace of growth for a spell, a plateau followed by more growth, or a temporary contraction.

None of these patterns will alter the fundamental trajectory of solar energy. But they will impact near and medium term market dynamics. If projects find themselves in need of new financing partners during these turbulent times, we’ll be here to help.

Concluding Thoughts

Despite some very good reasons to be optimistic about core policies supporting the US middle market, these are difficult developments. As of yet, we are not anticipating positives for the solar industry from GOP leadership. The conversation is all about anticipating the extent of the damage. Uncertainty makes these predictions especially difficult, but we’ve done our best to read the tea leaves here. And while we would prefer not to give Trump any more of the attention he seems to crave, it’s also important occasionally to address the elephant in the room.